Taxes on insurance premiums per year. Amounts of insurance premiums. Insurance premium for OPS

UST or unified social tax - this is what employers' insurance contributions for employees were previously called. In 2010, the unified social tax was abolished, but the term remained: many accountants, out of habit, continue to call insurance contributions “social tax.” What is the Unified Social Tax and in what form does it exist now, we will understand in the article.

Until 2010, the unified social tax was regulated by Chapter 24 of the Tax Code of the Russian Federation. Then this section of the law, as well as the tax itself, was abolished, and the administration of insurance payments was transferred to the Pension Fund of the Russian Federation, the Social Insurance Fund and the Compulsory Medical Insurance Fund.

In 2017, payments for compulsory insurance, except for contributions for injuries, were again transferred under the jurisdiction of the Federal Tax Service.

So what is the correct name for the unified social tax in 2018? Just “Insurance premiums”. They are regulated by Chapter 34 of the Tax Code of the Russian Federation.

Who pays insurance premiums (UST) in 2018

Everyone who uses hired labor. These are organizations and individual entrepreneurs who hire employees under employment contracts. All of them are required to pay contributions for four types of compulsory insurance:

- pension;

- medical;

- social;

- from accidents at work.

If an employee was hired under a civil contract to perform some work or services, contributions must be made only for pension and health insurance. Other taxes are by agreement of the parties. If you have any doubts about whether insurance premiums have been drawn up correctly and exactly what deductions need to be paid for a specific employee, consult with specialists. This will help prevent penalties and problems with the tax authorities in the future. If the company does not have a competent accountant on staff, we advise you to contact service professionals.

The employer makes all contributions at his own expense. It is illegal to shift the tax burden onto the employee, even if he agrees.

For more information on how individual entrepreneurs pay insurance premiums for themselves, read the article

Insurance premium rates (UST) in 2018, table

This table shows standard rates for 2018:

|

Insurance type |

Bid |

Regulatory document |

|

Mandatory pension insurance* |

clause 1 art. 426 Tax Code of the Russian Federation |

|

|

Compulsory health insurance |

clause 3 art. 426 Tax Code of the Russian Federation |

|

|

Compulsory social insurance in case of temporary disability and in connection with maternity** |

clause 2 art. 426 Tax Code of the Russian Federation |

|

|

Insurance against industrial accidents and occupational diseases |

from 0.2% to 8.5% |

Article 1 of Federal Law of December 22, 2005 N 179-FZ |

* If the employee’s annual income reaches the limit of RUB 1,021,000. The rate is reduced to 10% by the end of the year.

** If an employee’s annual income reaches the limit of 815,000 rubles, social insurance payments are not charged.

Deadlines for payment of insurance premiums (UST) in 2018

The deadline is the same for all types of insurance - until the 15th day of the month following the month of income accrual. If the 15th falls on a weekend, the deadline is moved to the next working day after it.

Reduced insurance premium rates

Detailed information about who is entitled to reduced rates in 2018 and under what conditions the benefit can be applied is contained in Article 427 of the Tax Code of the Russian Federation.

Here are the most common categories of beneficiaries:

- Entrepreneurs and organizations on the simplified tax system that are engaged in the types of activities listed in clause 5 of clause 1 of Art. 427 Tax Code of the Russian Federation.

- Entrepreneurs on the patent system in relation to payments to employees engaged in activities that are specified in the patent (except rental, retail and catering).

- Organizations and entrepreneurs on UTII who conduct pharmacy (pharmaceutical) activities.

For all the employers listed above, in 2018 the pension insurance tariff is 20%, and the social and medical insurance tariff is 0%.

Unfortunately, in 2019 this benefit will no longer apply to them - the period of validity of the reduced tariffs was not extended.

The Ministry of Finance of the Russian Federation, in its letter No. 03-15-06/54260 dated August 1, 2018, also announced that the extension of benefits for small businesses engaged in the production and social spheres is not provided for in the budget.

For the remaining beneficiaries specified in Article 427 of the Tax Code of the Russian Federation, the benefits will continue to apply, but with minor changes.

Upcoming changes in insurance premiums

In addition to the abolition of benefits, employers will face the following changes in 2019:

The limit for contributions to pension insurance will change to 1,150,000 rubles, for payments to social insurance – to 865,000 rubles.

The 22% tariff for pension insurance will become permanent. Before this, the general tariff was 26%, and the 22% rate was supposed to be in effect only in 2017-2020.

Fixed contributions of entrepreneurs for themselves will also increase.

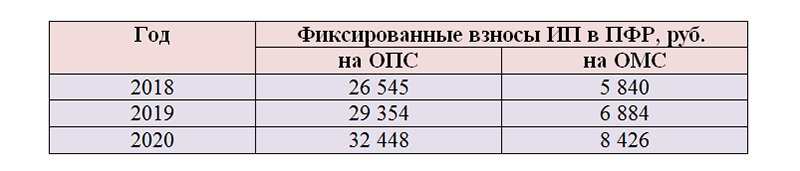

In 2019, individual entrepreneurs will have to pay for themselves:

RUB 29,354 for compulsory pension insurance;

RUB 6,884 for compulsory health insurance.

Nothing changes regarding the 1% payment on income over 300 thousand rubles.

The maximum payment amount for individual entrepreneurs for OPS in 2019 will be 234,832 rubles. (8 × 29,354 rub.).

In addition, in 2019, individual entrepreneurs who want to voluntarily pay insurance premiums for themselves in case of temporary disability and in connection with maternity will have to pay 3,925.44 rubles to the budget of the Federal Social Insurance Fund of Russia.

The amounts of insurance premiums and benefits change all the time and it is sometimes very difficult to track innovations. Confusion about tax rates can lead to penalties. Understanding the intricacies of insurance premiums and paying all taxes on time is not difficult if you enlist the support of professionals. Service employees will help you understand tax reforms and take charge of communication with the tax office. Try it - it's very convenient!

How to save on insurance premiums

There are few legal ways, but they exist.

For example, you can conclude with a potential employee not an employment contract, but a student agreement. Scholarships under a student agreement are not subject to insurance contributions.

Article 422 lists payments that are not subject to insurance contributions. Part of an employee's salary can be replaced with these payments. Thus, financial assistance up to 4 thousand rubles per year, financial assistance for the birth and adoption of a child up to 50 thousand rubles per child, daily allowance in any amount and compensation for travel expenses, etc. are not taxed.

If you use the services of individuals under civil contracts, in addition to personal income tax, you must pay 22% of pension contributions and 5.1% of medical contributions from the remuneration under this contract. Look for a person who provides the same services, but is registered as an individual entrepreneur. Enter into an agreement with him as an individual entrepreneur, and then he will pay taxes and contributions for himself.

Let's consider the procedure for calculating and paying insurance premiums in 2018. See the calculation of the maximum taxable base for certain types of insurance for 2018 based on the Tax Code of the Russian Federation.

From January 1, 2018, insurance premiums will increase. In the article you will find a table of insurance premium rates, new base limits and deadlines for paying insurance premiums in 2018.

Insurance premiums in 2018: rates table

The amount of insurance premiums for 2018 will not change. The general insurance premium rate for 2018 is 30 percent. Payers make deductions for insurance premiums within the established maximum amount of the taxable base at the previous rates:

- 22% – contributions to compulsory pension insurance (OPI).

- 5.1% – contributions for compulsory health insurance (CHI).

- 2.9% – contributions to compulsory social insurance (OSS).

Such tariffs must be applied until the employee’s income on an accrual basis from the beginning of the year does not exceed the maximum base. And from the excess amount, contributions must be calculated at the following rates:

- 10% – pension contributions,

- 5.1% – medical contributions,

- 0% – contributions in case of illness and maternity.

On a note

The general rate of 30% for insurance premiums will be valid until 2020 inclusive (Law No. 361-FZ dated November 27, 2017).

The rate for the contribution for injuries is set individually for each organization. Its rate is determined by the professional risk class assigned to the organization. For the first, the contribution amount is 0.2%, for the last, thirty-second – 8.5%. If an organization has been operating for three years without injuries or other violations in the field of labor protection, it can receive a discount of up to 40% of the tariff. At the same time, the fund will check the conduct of a special assessment of workplaces and the organization of mandatory medical examinations.

Table 1 shows the rates of insurance premiums for 2018 depending on the maximum value of the base.

Table 1. Table of rates (tariffs) of insurance premiums in 2018

Let's give an example of how to determine the rate and calculate insurance premiums in 2018.

The salary of the Vice-Rector of the State Institution “University” I.F. Baryshnikov is 70,000 rubles. In December, the accountant accrued 200,000 rubles to the vice-rector. awards.

The institution applies general insurance premium rates. The premium rate for insurance against accidents and occupational diseases is 0.2%. The accountant calculated the amount of contributions as follows.

The taxable base from April 1 to December 31 will be 1,040,000 rubles. (RUB 70,000 × 12 months + RUB 200,000).

Baryshnikov has a single tax base for both pension and social contributions.

In December, the taxable base will exceed the limit:

- for pension contributions by 19,000 rubles. (1,040,000 – 1,021,000);

- social contributions for 225,000 rubles. (1,040,000 –815,000).

- for pension contributions – 251,000 rubles. (70,000 + 200,000 – 19,000);

- social contributions – 45,000 rubles. (70,000 + 200,000 – 225,000).

Accrued contributions at general rates from payments for December, which do not exceed the maximum amount.

- pension contributions amounted to 55,220 rubles (251,000 rubles × 22%);

- social contributions – 1305 rub. (RUB 45,000 × 2.9%).

There is no need to pay social contributions in excess.

Changes in insurance premiums since 2018

The following changes occurred in insurance premiums in 2018:

- The size of the maximum base for OPS and OSS has been increased;

- Several income codes have been changed to which certain types of payments are credited;

- Amendments have been made to the article of the Tax Code of the Russian Federation regulating the application of reduced tariffs.

From January 6, 2018, changes were made to the procedure for financing preventive measures in the field of labor protection through contributions to compulsory accident insurance. In order to receive compensation for purchased workwear, personal protective equipment, and safety shoes, you must present a copy of the conclusion of the Ministry of Industry and Trade confirming the production of these products in the Russian Federation. Fabric and other materials used in production must also be Russian.

Limit base for insurance premiums in 2018

The government increased the limit for calculating insurance premiums in 2018 (Resolution of the Government of the Russian Federation dated November 15, 2017 No. 1378). At the same time, the main provision remained unchanged; the maximum base was established only for contributions to the Pension Fund and the Social Insurance Fund. And contributions for health insurance and injuries are taken from any amount.

The maximum base for insurance premiums in 2018 is equal to:

- for social insurance – 815 thousand rubles,

- pension insurance – 1,021 thousand rubles.

The maximum base for calculating insurance premiums in 2018 for compulsory medical insurance and insurance from NS and PZ is not established. From earnings exceeding the legal maximum, 10% is taken for pension insurance. For social insurance, all accruals are made only up to the upper limit.

Table 2. New limits on insurance premiums for 2018

Check the calculation of insurance premiums using the Federal Tax Service formulas.

Deadlines for payment of insurance premiums in 2018

Insurance premiums must be paid no later than the 15th of the following month. This is a requirement of Article 34 of the Tax Code of the Russian Federation. If the due date falls on an official holiday, the payment deadline is postponed to the next working day.

Contributions are considered paid at the time the payment order is submitted to the bank. In this case, two conditions must be met:

- The order is filled out without errors;

- There is a sufficient amount of funds in the payer's account.

Table 3. Deadlines for payment of insurance premiums in 2018

Payment of insurance premiums in 2018

The budget classification code is a required field that is filled in when paying contributions. In the payment order, KBK is indicated in field 104. Contributions for employees to the Federal Tax Service in 2018 must be paid for each type of insurance.

On April 23, 2018, Order No. 35n of the Ministry of Finance dated February 28, 2018 came into effect. He amends the BCC to include in the budget penalties and fines on contributions to compulsory pension insurance transferred for employees entitled to early retirement. Article 428 of the Tax Code provides for differentiation of the additional tariff rate depending on whether a special assessment of working conditions has been carried out at the workplaces of these workers or not. Amounts of contributions accrued at different rates were transferred to separate BCCs.

There was no such gradation for penalties and fines. They were listed using the same code, regardless of what rate was applied to the late payment: with or without a special assessment. From April 23, 2018, new BCCs were introduced for the payment of penalties and fines at an additional tariff. The table shows the current budget classification codes taking into account innovations.

Table 4. Payment of insurance premiums in 2018

|

Name of contributions |

|||

|

1821020201061010160 |

18210202010062110160 |

18210202010063010160 |

|

|

18210202090071010160 |

18210202090072110160 |

18210202090073010160 |

|

|

18210202101081013160 |

18210202101082013160 |

18210202101083013160 |

|

|

Add. tariff 1 without special rate |

18210202131061010160 |

18210202131062110160 |

18210202131063010160 |

|

Add. tariff 1 with special price |

18210202131061020160 |

18210202131062100160 |

18210202131063000160 |

|

Add. tariff 2 without special rate |

18210202132061010160 |

18210202132062110160 |

18210202132063010160 |

|

Additional rate 2 with special price |

18210202132061020160 |

18210202132062100160 |

18210202132063000160 |

|

OPS fixed size |

18210202140061110160 |

18210202140062110160 |

1821020214006010160 |

|

Compulsory medical insurance fixed size |

18210202103081013160 |

18210202103082013160 |

18210202103083013160 |

|

Insurance against accidents and damages |

39310202050071000160 |

39310202050072100160 |

39310202050073000160 |

For contributions to pension insurance in a fixed amount, which are paid by individual entrepreneurs, from April 23, 2018, one BCC is applied, it is indicated in the table. In the old version, contributions calculated from income up to 300 thousand rubles. and exceeding 300 thousand rubles were transferred to different budget income codes.

If you have any questions about using KBK codes, please use. In the service, you can determine the BCC for a payment or find out the type of payment for a specific BCC.

Reduced insurance premium rates in 2018

The Tax Inspectorate plans to provide users reporting electronically with additional options for document control at the sending stage. Those errors that the Federal Tax Service has detected will be able to be seen and corrected independently.

The insurance premium rate for 2018 is established by law, and certain types of rates have changed since the beginning of the year. We will talk about these changes and other nuances of insurance rates in the article below.

Payers of insurance premiums are listed in Art. 419 Tax Code of the Russian Federation:

For more information about insurance premium payers, see this publications .

Legislation in the field of insurance premiums is periodically adjusted, and officials of the Ministry of Finance and the Federal Tax Service interpret it in their own way. Here are some of the changes (actual and planned) and clarifications:

- From 01/01/2018, individual entrepreneurs’ contributions to the Pension Fund are not tied to the level of the minimum wage and are fixed in the form of fixed amounts for the coming years (2018-2020) in Art. 430 Tax Code of the Russian Federation:

- Officials of the Ministry of Finance in a letter dated 02.12.2018 No. 03-15-07/8369 (sent by a letter of the Federal Tax Service dated 02.21.2018 No. GD-4-11/3541@) prohibited individual entrepreneurs under special regimes (STS, UTII and patent) from reducing income received for expenses when calculating contributions. And only individual entrepreneurs on the general taxation system are allowed to do this. At the same time, the Federal Tax Service previously confirmed the possibility of simplifiers using the “income minus expenses” object to pay 1% to the Pension Fund of the Russian Federation on the difference between income and expenses (review of the legal positions of the Constitutional and Supreme Courts, approved by the Federal Tax Service of Russia on January 23, 2018).

- It is likely that soon policyholders will have to prepare reports on contributions (ERSV) on an updated form (at the time of writing, the draft order of the Federal Tax Service is at the stage of public discussion).

- It is planned that residents of TOP (advanced development territories) and residents of the free port of Vladivostok will be able to apply reduced rates on insurance premiums for 10 years from the period of acquiring such status.

Find out about tax innovations from our .

Groups of insurance rates

The insurance premium rate is the rate established by law by which the insurer’s obligations are calculated. Each type of contribution has its own tariff.

Conventionally, insurance premium rates can be divided into 4 groups:

- percentage - set as a percentage of the insurance premium base (for example: 22%, 5.1%, etc.);

- total - indicated in fixed amounts without reference to the base of insurance premiums (for example, fixed contributions of individual entrepreneurs for themselves);

- combined - are a combination of a percentage rate and a sum rate (for example, the rate of contributions for individual entrepreneurs for themselves with an income of more than 300,000 rubles).

Tariffs for insurance premiums for 2018 are presented for clarity in the form of a table/diagram using information from the Tax Code of the Russian Federation for each type of contribution according to the following items:

- 426 (basic tariffs for the current year);

- 427 (reduced insurance premium rates in 2018);

- 428, 429 (additional tariffs).

Separate additional tariffs are provided for in Art. 429 of the Tax Code of the Russian Federation for social security of flight crew members of civil aviation aircraft and certain categories of employees of coal industry companies.

The completeness, correctness and timeliness of payment of the above insurance premiums are supervised by tax officials.

Contribution rates according to Law No. 125-FZ

According to the law on compulsory insurance against industrial accidents and occupational diseases dated July 24, 1998 No. 125-FZ, contributions “for injuries” are paid .

These are mandatory payments transferred by policyholders to the Social Insurance Fund. Of these, individuals are paid compensation for harm to health (received while performing work duties).

This type of insurance premium (unlike those listed above) is not controlled by the tax authorities. They are supervised by social insurance.

The difference between this type of contribution and other mandatory insurance premiums lies in the special technology for determining them (individual approach).

The rates of insurance premiums for 2018 “for injuries” can be found in Art. 1 of the Law of December 22, 2005 No. 179-FZ. The fact that they are still relevant in 2018 is stated in Art. 1 of the Law of December 31, 2017 No. 484-FZ.

In 2018 (as in previous years), 32 contribution rates “for injuries” are in effect - a separate rate for each class of professional risk.

The rate of contributions “for injuries” differs from other insurance premiums in the specific way they are established:

- for each policyholder, tariffs are set annually by social insurance specialists;

- their value depends on the occupational risk class of the organization’s main activity;

- the main type of activity must be confirmed by submitting to the Social Insurance Fund (annually no later than April 15) a package of documents (application for confirmation of the main type of activity, a confirmation certificate and a copy of the explanations to the balance sheet);

- in the absence of this package of documents, the fund’s specialists will independently set the contribution rate based on the type of activity with the highest class of professional risk.

Let's look at an example of how the rate of contributions “for injuries” depends on the presence/absence of confirmation of the main type of activity.

See how timely confirmation of the company’s main activity affects the rate.

Example 1

StroyProekt LLC received revenue last year in the following amount (by type of activity):

* The specialists of StroyProekt LLC took the occupational risk class from the appendix to the Order of the Ministry of Labor dated December 30, 2016 No. 851n.

** The rate of contributions “for injuries” is indicated in accordance with Art. 1 of the Law of December 22, 2005 No. 179-FZ.

Conclusion: the main activity of StroyProekt LLC is construction design - OKVED 41.10 (largest share of revenue: 31.24%). The insurance premium rate is 0.2.

No later than 04/16/2018 (rescheduled from Sunday, 04/15/2018), StroyProekt LLC should send the necessary papers to the FSS to confirm the main type of activity.

Find out how the Social Insurance Fund feels about postponing reporting deadlines from the publication.

Example 2

Let's change the conditions of example 1: StroyProekt LLC did not confirm the main type of activity.

As a result, the fund’s specialists independently established the insurance premium rate “for injuries” for StroyProekt LLC, choosing the maximum rate - 1.2.

Conclusion: the absence in the Social Insurance Fund of documents confirming the main activity of StroyProekt LLC has led to a situation where the company will have to pay contributions in an amount 6 times higher than the “confirmed” tariff.

Tariffs for entrepreneurs

Individual entrepreneurs calculate and pay contributions according to two schemes:

- as employers (calculating insurance premiums from the income of their employees);

- for yourself (regardless of whether the individual entrepreneur has employees or not).

At the same time, the individual entrepreneur pays contributions to compulsory health insurance and contributions to health insurance for himself. This concludes the mandatory part for insurance premiums for individual entrepreneurs. But there remains the possibility of voluntarily paying contributions as part of insurance in the event of disability or in connection with maternity. When paying such contributions, the entrepreneur has the right to receive benefits upon the occurrence of an insured event (illness or childbirth).

We talk about modern types of sick leave certificates in the articles:

- ;

Find out more about insurance premium rates for 2018 for individual entrepreneurs in the next section.

Combined tariff formula for individual entrepreneurs

Tariffs for compulsory pension insurance (OPI) from 2018:

- established in the form of a fixed payment (if the individual entrepreneur’s income does not exceed 300,000 rubles);

- are calculated in a combined way for income over 300,000 rubles. (fixed payment + percentage of excess income over the amount of 300,000 rubles).

In 2018, insurance premiums for OPS (SV OPS) are calculated as follows (subclause 1, clause 1, Article 430 of the Tax Code of the Russian Federation):

If D ≤ 300,000 rub. → SV OPS = 26,545 rub.

If D > 300,000 rub. → SV OPS = 26,545 rub. + 1% × [D - 300,000 rub.]

At the same time, the MV of the compulsory pension insurance for the billing period cannot exceed 8 times the fixed amount of insurance premiums for the compulsory pension insurance.

In other words, if the income of an individual entrepreneur for 2018 did not exceed 300,000 rubles, he does not need any calculations. He will take the amount of insurance premiums for compulsory insurance from the Tax Code of the Russian Federation: 26,545 rubles. If the limit is 300,000 rubles. exceeded, it is impossible to do without calculation. For an example of such a calculation, see below.

Calculation of contributions using the combined tariff formula

Let's look at the calculation of pension contributions for individual entrepreneurs with income in 2018 exceeding 300,000 rubles.

Example 3

Individual Entrepreneur E.T. Krasilnikov applies a general taxation system and works without the involvement of hired labor. Its performance indicators in 2018:

- income - 5,638,339 rubles;

- expenses - 4,060,788 rubles.

Thus, to calculate contributions to compulsory pension insurance, the income of individual entrepreneur E.T. Krasilnikov (reduced by the amount of expenses) amounted to 1,577,551 rubles. (5 638 33 - 4 040 788).

Since RUB 1,577,551 exceeds 300,000 rubles, E.T. Krasilnikov needs to apply the formula to calculate the amount of contributions to the compulsory pension insurance for 2018:

SV OPS = 26,545 + 1%× (1,577,551-300,000) = 42,321 rubles.

Insurance premiums regulated by the norms of Ch. 34 of the Tax Code of the Russian Federation will be applied in 2018 with adjustments made on New Year's Eve. Since for the second year they will be administered by tax authorities in accordance with the Tax Code of the Russian Federation, this is not a surprise for insurance premium payers: tax legislation is being reformed continuously.

Read about changes in the procedure for calculating and paying insurance premiums that need to be taken into account in 2018 in the proposed material.

The maximum value of the base for insurance premiums in 2018.

For insurance premium payers making payments to individuals, a maximum base value for calculating insurance premiums is established:

for compulsory pension insurance (OPI);

for compulsory social insurance in case of temporary disability and in connection with maternity.

Since the base for insurance premiums is determined by an accrual total from the beginning of the billing period, from the amounts of payments and other remuneration in favor of an individual exceeding the established maximum value of the base for calculating insurance premiums, as a general rule, insurance premiums are not charged (clause 3 of Article 421 of the Tax Code of the Russian Federation ).

Chapter 34 of the Tax Code of the Russian Federation establishes a certain procedure for calculating the maximum amount of the base for insurance premiums, which is established annually by the Government of the Russian Federation, which was done for 2018 by Decree of the Government of the Russian Federation dated November 15, 2017 No. 1378 (see table).

Let us remind you that for insurance premiums for compulsory medical insurance (CHI), no maximum base size is established; accordingly, these insurance premiums are calculated regardless of the amount of payments in favor of an individual.

Insurance premium rates for 2018. General rates of insurance premiums.

According to Art. 426 of the Tax Code of the Russian Federation in 2017 - 2019, the following insurance premium rates apply:

within the established maximum value of the base for calculating insurance premiums for compulsory health insurance – 22%;

above the established maximum base for calculating insurance premiums for compulsory health insurance – 10%;

2) for compulsory social insurance in case of temporary disability and in connection with maternity within the established maximum value of the base for calculating insurance premiums for this type of insurance - 2.9%;

3) for compulsory social insurance in case of temporary disability in relation to payments and other remuneration in favor of foreign citizens and stateless persons temporarily staying in the Russian Federation (with the exception of highly qualified specialists), within the established maximum value of the base for calculating insurance premiums for this type of insurance – 1.8%;

4) for compulsory medical insurance – 5.1%.

Federal Law No. 361-FZ dated November 27, 2017 extended the validity of the tariffs established by Art. 426 of the Tax Code of the Russian Federation, for 2020 inclusive.

Thus, the total amount of insurance premiums of 30% within the established limit values of the base for calculating insurance premiums and in the amount of 10% for compulsory public health insurance in excess of the established limit value of the base for calculating insurance premiums for compulsory public health insurance is maintained for the next three years.

Tariffs of insurance premiums for residents of the SEZ of the Kaliningrad region.

Federal Law No. 353-FZ dated November 27, 2017 “On Amendments to Part Two of the Tax Code of the Russian Federation” amended Art. 427 of the Tax Code of the Russian Federation: since 2018, organizations included in the unified register of residents of the Special Economic Zone in the Kaliningrad Region in accordance with Federal Law No. 16-FZ dated January 10, 2006 (SEZ of the Kaliningrad Region) apply reduced insurance premium rates.

The specified payers of insurance premiums, within the established maximum value of the base for calculating insurance premiums for the corresponding type of insurance, apply the following reduced rates of insurance premiums (clause 5, clause 2, article 427 of the Tax Code of the Russian Federation):

for OPS – 6%;

for compulsory social insurance in case of temporary disability and in connection with maternity – 1.5%;

for compulsory medical insurance – 0.1%.

The specifics of applying reduced tariffs in this case are established in clause 11 of Art. 427 Tax Code of the Russian Federation. If insurance premium payers do not fulfill these conditions, they will not have the right to apply reduced insurance premium rates.

Reduced insurance premium rates for residents of the Kaliningrad region SEZ are applied taking into account the following features:

the payer of insurance premiums must be included in the unified register of residents of the SEZ of the Kaliningrad region in the period from January 1, 2018 to December 31, 2022 inclusive;

reduced tariffs are applied for seven years starting from the 1st day of the month following the month in which such a payer was included in the register, but not more than the deadline;

the deadline for applying reduced tariffs for payers is set until December 31, 2025;

in case of exclusion of payers from the register, reduced tariffs are not applied from the 1st day of the month following the month in which payers were excluded from the register;

reduced tariffs are applied by payers exclusively in relation to the base for calculating insurance premiums determined in relation to individuals employed in new jobs.

In this case, the legislator clearly defined what is meant by a new workplace: this is a place created for the first time by organizations included in the register when implementing an investment project on the territory of a special economic zone in the Kaliningrad region. In this case, an individual employed in a new workplace is recognized as a person who has entered into a contract with an organization included in the register, and his labor duties are directly related to the implementation of the specified investment project, including the operation of fixed assets created as a result of the implementation of the investment project. The list of payers' workplaces related to new jobs is approved by payers before the application of reduced insurance premium rates in agreement with the administration of the SEZ in the Kaliningrad region and the tax authority at the location of the payers.

The establishment of reduced tariffs for insurance premiums is one of the directions for creating a favorable tax regime for the development of economic and scientific potential in the Kaliningrad region, attracting investment in the regional economy, as well as creating a financial base for the accelerated socio-economic development of the Kaliningrad region.

Features of the application of reduced insurance premium rates in 2018.

Federal Law No. 335-FZ of November 27, 2017 “On Amendments to Parts One and Two of the Tax Code of the Russian Federation and Certain Legislative Acts of the Russian Federation” (hereinafter referred to as Federal Law No. 335-FZ) introduced a number of changes to Art. 427 of the Tax Code of the Russian Federation, which regulates the procedure for applying reduced insurance premium rates.

“Simplers” carrying out activities in the social and industrial fields. In accordance with paragraphs. 5 p. 1 art. 427 of the Tax Code of the Russian Federation, reduced rates of insurance premiums can be applied by organizations and individual entrepreneurs using the simplified tax system and carrying out established types of activities.

Action of paragraphs. 5 p. 1 art. 427 of the Tax Code of the Russian Federation in the new edition applies to legal relations that arose from January 1, 2017.

In the new edition of paragraphs. 5 p. 1 art. 427 of the Tax Code of the Russian Federation provides new “old” types of activities in respect of which “simplified” have the right to apply reduced rates of insurance premiums if the established conditions are met. So, are new or old types of activities now allowing “simplified” people to apply lower insurance premium rates? Let's figure it out.

In the new edition of paragraphs. 5 p. 1 art. 427 of the Tax Code of the Russian Federation provides a list of types of activities in the social and industrial areas, and it applies to 2017. Thus, one of the problems of the “simplified” people, whose name of the type of economic activity has changed due to the introduction of the new All-Russian Classifier of Types of Economic Activities (OKVED 2), has been resolved.

Based on the provisions of paragraphs. 5 clause 1, pp. 3 clause 2 and clause 6 art. 427 of the Tax Code of the Russian Federation for payers of insurance premiums using the simplified tax system, the main type of economic activity (classified on the basis of activity codes in accordance with the All-Russian Classifier of Types of Economic Activities) of which is activity in the social and industrial areas, for the period up to 2018 (inclusive) an aggregate reduced rate of insurance premiums in the amount of 20% while simultaneously meeting the conditions on the maximum amount of income for (not more than 79 million rubles) and the share of income from sales of products and (or) services provided in the main type of economic activity in total income (not less than 70 %).

At the same time, the established list of types of economic activities is enlarged and includes both types of activities combined into one class, subclass, group, subgroup of the classifier, and individual types of economic activities with the corresponding names in the specified list.

By order of Rosstandart dated January 31, 2014 No. 14-st, a new edition of the All-Russian Classifier of Economic Activities - OKVED OK 029-2014 (NACE Rev. 2) (OKVED 2) came into force on January 1, 2017, with OKVED OK 029-2001 ( NACE Rev. 1) (OKVED 1) is no longer valid.

Logically, the introduction of OKVED 2 from January 1, 2017 should not have entailed the loss by some payers of the right to apply reduced insurance premium rates established by the provisions of Art. 427 Tax Code of the Russian Federation. However, as a result of the introduction of OKVED 2, which entailed the restructuring of sections of the All-Russian Classifier of Types of Economic Activities, a number of insurance premium payers who carried out activities in the industrial and social fields before the designated date and continue to currently carry out activities in the industrial and social fields have changed the name of the type of economic activity, and some of the preferential types activities in accordance with OKVED 1 were included in other types of activities in accordance with OKVED 2. Accordingly, such payers lost the right to apply reduced insurance premium rates.

At the same time, representatives of the Ministry of Finance explained that if, before 2017, “simplified people” could apply reduced insurance premium rates on the specified grounds, then they have the right to do this in 2017, regardless of the coincidence or discrepancy of activity codes according to OKVED 2 according to the applied keys (Letter of the Ministry of Finance Russia dated October 13, 2017 No. 03-15-07/66964, communicated to the territorial tax authorities by Letter of the Federal Tax Service of Russia dated October 25, 2017 No. GD-4-11/21578@). But these were just clarifications.

And now the list of these types of activities has actually been reduced to the original version, which corresponds to the current OKVED 2.

Thus, “simplers” who temporarily lost the right to apply reduced insurance premium rates in 2017 can recalculate insurance premiums for 2017 and submit updated calculations, and in 2018 have the full right to apply reduced insurance premium rates.

In addition, it is clarified that when calculating the share of income, the total amount of income is determined by summing the income specified in paragraph 1 and paragraphs. 1 clause 1.1 art. 346.15 of the Tax Code of the Russian Federation, that is, income from sales, non-operating income, as well as income indicated in Art. 251 of the Tax Code of the Russian Federation, which are not taken into account when determining the object of taxation under the simplified tax system. This rule has also been in effect since 2017.

Organizations that operate in the field of information technology.

Russian organizations that operate in the field of information technology should pay attention to the fact that in paragraph 5 of Art. 427 of the Tax Code of the Russian Federation the following amendment has been made: reference to paragraphs. 1 item 2 art. 427 was replaced throughout the paragraph by paragraphs. 1.1 clause 2 art. 427 Tax Code of the Russian Federation. And these innovations are extended to legal relations that arose from January 1, 2017. Fundamentally, nothing changes for these insurance premium payers, since the typo has actually been corrected.

Non-profit organizations using the simplified tax system.

Non-profit organizations applying the simplified tax system and carrying out socially significant types of activities have the right to apply reduced rates of insurance premiums, provided that at the end of the year preceding the year the organization switched to paying insurance premiums at such rates, at least 70% of the amount of all income of the organization for the specified period is in total the following types of income:

- income from carrying out the types of economic activities specified in paragraph. 17 – 21, 34 – 36 pp. 5 p. 1 art. 427 Tax Code of the Russian Federation.

income in the form of targeted revenues for the maintenance of non-profit organizations and their conduct of statutory activities in accordance with paragraphs. 7 clause 1 art. 427 of the Tax Code of the Russian Federation, determined in accordance with paragraph 2 of Art. 251 of the Tax Code of the Russian Federation (targeted revenues);

income in the form of grants received for carrying out activities on the basis of paragraphs. 7 clause 1 art. 427 of the Tax Code of the Russian Federation and determined on the basis of paragraphs. 14 clause 1 art. 251 Tax Code of the Russian Federation (grants);

So, starting from 2017, targeted revenues and grants remained unchanged in this list, and the third component - types of activities - was replaced (paragraphs 47, 48, 51 - 59, paragraph 5, clause 1, article 427 of the Tax Code of the Russian Federation). In general, the types of activities have not changed, including scientific research and development, education, healthcare and the provision of social services, the activities of sports facilities, but there are still some point changes, so it is advisable for non-profit organizations to once again clarify the names of types of activities in accordance with the new OKVED 2 for the purposes of applying reduced insurance premium rates.

In addition, it is noted that when calculating the share of income, the total amount of income is determined by summing the income specified in paragraph 1 and paragraphs. 1 clause 1.1 art. 346.15 of the Tax Code of the Russian Federation, that is, income from sales, non-operating income, as well as income referred to in Art. 251 of the Tax Code of the Russian Federation, which are not taken into account when determining the object of taxation under the simplified tax system.

The changes discussed have also been in effect since 2017.

Object of taxation of insurance premiums.

Federal Law No. 335-FZ amended Art. 420 of the Tax Code of the Russian Federation, which come into force on January 1, 2018.

Exclusive rights to works of science, literature, art.

As a general rule, the object of taxation of insurance premiums is payments and other remuneration in favor of individuals within the framework of labor relations and under civil law contracts, under copyright contracts in favor of the authors of works, as well as under agreements on the alienation of exclusive rights and licensing agreements. In the new edition of Art. 420 Tax Code of the Russian Federation, paragraphs. 3 clause 1 reformulated: under alienation agreements exclusive right to the results of intellectual activity specified in paragraphs. 1 – 12 p. 1 tbsp. 1225 Civil Code of the Russian Federation, publishing license agreements, license agreements for the provision the right to use the results of intellectual activity specified in paragraphs. 1 – 12 p. 1 tbsp. 1225 Civil Code of the Russian Federation, including remunerations accrued by rights management organizations on a collective basis in favor of authors of works under agreements concluded with users.

These innovations are associated with bringing the Tax Code of the Russian Federation into conformity with the Civil Code of the Russian Federation.

Similar changes were made to paragraph 4 of Art. 420 of the Tax Code of the Russian Federation, as well as clause 8 of Art. 421 and paragraphs. 2 p. 3 art. 422, which indicate, respectively, payments and the base recognized and not recognized as the object of taxation by insurance premiums.

Individual entrepreneurs.

The object of taxation of insurance premiums for individual entrepreneurs, lawyers, mediators, notaries, arbitration managers, appraisers, patent attorneys and other persons engaged in private practice in accordance with the procedure established by the legislation of the Russian Federation (hereinafter referred to as individual entrepreneurs) is the minimum wage (minimum wage) established at the beginning of the corresponding billing period, in the case provided for in paragraph. 3 pp. 1 clause 1 art. 430 of the Tax Code of the Russian Federation, the object of taxation of insurance premiums is also recognized as income received by the payer of insurance premiums and determined in accordance with clause 9 of Art. 430 Tax Code of the Russian Federation.

That is, individual entrepreneurs (and other specified persons) paid insurance premiums for themselves, based on the size of the minimum wage, as well as if their income exceeded 300,000 rubles. – additional 1% of the amount of income on OPS.

Since 2018, this rule has changed: now the size of insurance premiums will no longer depend on the minimum wage (see below).

Base for calculating insurance premiums

The procedure for determining the base for calculating insurance premiums is established by Art. 421 of the Tax Code of the Russian Federation, which has been in force since January 1, 2018 in a new edition:

clause 8 art. 421 of the Tax Code of the Russian Federation has been brought into conformity with the norms of the Civil Code of the Russian Federation (see above);

Certain cost norms have been adjusted, which can be accepted when calculating insurance premiums if the costs are not supported by documents (clause 9 of Article 421 of the Tax Code of the Russian Federation).

Here are the amended norms of paragraphs. 9 tbsp. 421 Tax Code of the Russian Federation. If the expenses specified in clause 8 of Art. 421 of the Tax Code of the Russian Federation cannot be supported by documents; they are accepted for deduction in the following amounts (as a percentage of the amount of accrued income):

for the creation of audiovisual works (video, television and cinema films), phonograms, broadcast messages or cable radio or television broadcasts - 30%;

for the creation of scientific works and developments, computer programs, databases - 20%;

for discoveries, selection achievements, inventions, creation of utility models, industrial designs, production secrets (know-how), topologies of integrated circuits (percentage of the amount of income received in the first two years of use) - 30%.

The amount and procedure for calculating and paying insurance premiums paid by individual entrepreneurs for themselves

Since 2018, the procedure for calculating insurance premiums for themselves by individual entrepreneurs and other persons engaged in private practice has fundamentally changed: Federal Law No. 335-FZ amended Art. 430 Tax Code of the Russian Federation.

In 2017, insurance premiums paid by individual entrepreneurs for themselves for compulsory health insurance and compulsory medical insurance were calculated on the basis of the minimum wage.

Since 2018, a new procedure has been in effect: individual entrepreneurs, as well as heads (and members) of peasant (farm) households, pay insurance premiums in a fixed amount (see table).

At the same time, as before, the amount of insurance premiums for compulsory health insurance and compulsory medical insurance as a whole for a peasant (farm) farm is determined as the product of a fixed amount for the billing period and the number of all members of the peasant (farm) farm, including the head of the peasant (farm) farm.

|

Insurance premiums |

Fixed amount of insurance premiums |

||

|---|---|---|---|

|

Individual entrepreneurs |

|||

|

Insurance premiums for OPS: |

|||

|

the payer’s income for the billing period does not exceed 300,000 rubles. |

|||

|

the payer’s income for the billing period exceeds 300,000 rubles. |

RUB 26,545 + 1% of the payer’s income exceeding RUB 300,000. for the billing period |

RUB 29,354 + 1% of the payer’s income exceeding RUB 300,000. for the billing period |

RUB 32,448 + 1% of the payer’s income exceeding RUB 300,000. for the billing period |

|

Maximum amount of insurance premiums for compulsory health insurance |

(RUB 26,545 x 8) |

(RUB 29,354 x 8) |

(RUB 32,448 x 8) |

|

Insurance premiums for compulsory medical insurance |

|||

|

Peasant (farm) farms |

|||

|

Insurance premiums for OPS |

|||

|

Insurance premiums for compulsory medical insurance |

|||

Let us remind you that for 2017, individual entrepreneurs are required to pay insurance premiums for themselves in the following amounts (Letter of the Federal Tax Service of Russia dated 03/07/2017 No. BS-4-11/4091@). On OPS:

if the payer’s income does not exceed 300,000 rubles. for the billing period - in the amount defined as 1 minimum wage (RUB 7,500 for 2017) x 26% x 12 months. = 23,400 rub.;

if the payer’s income exceeds RUB 300,000. for the billing period - in the amount defined as 1 minimum wage (RUB 7,500 for 2017) x 26% x 12 months. + 1% of the amount of income of the payer of insurance premiums exceeding RUB 300,000.

In this case, the amount of insurance premiums paid by the payer cannot exceed the amount defined as 8 minimum wages (RUB 7,500 for 2017) x 26% x 12 months. = 187,200 rub.

The amount of insurance premiums for compulsory medical insurance for the billing period is determined as 1 minimum wage (RUB 7,500 for 2017) x 5.1% x 12 months. = 4,590 rub.

Since 2018, the calculation of insurance premiums for compulsory health insurance and compulsory health insurance for individual entrepreneurs for themselves has changed fundamentally: the amount of insurance premiums no longer depends on the minimum wage, a fixed amount has been established for the next three years. At the same time, the threshold value of income of 300,000 rubles, from which an additional percentage of insurance premiums for compulsory health insurance is paid, has not changed, and the maximum amount of insurance premiums for compulsory health insurance has remained in the form of 8 times the fixed amount.

In addition to the above innovations, clause 7 of Art. 430 of the Tax Code of the Russian Federation, which indicates cases of exemption of individual entrepreneurs from paying insurance premiums: it is clarified that entrepreneurs are required to submit applications for exemption from paying insurance premiums and supporting documents to the tax authority at the place of registration. This is not a new condition; in practice, tax authorities have required supporting documents before, they were supported by representatives of the Ministry of Finance (Letter No. 03-15-05/61112 dated September 21, 2017).

Another change for individual entrepreneurs will be new deadlines for payment of insurance premiums (clause 2 of Article 432 of the Tax Code of the Russian Federation):

the amounts of insurance premiums for the billing period are paid by payers no later than December 31 of the current calendar year. This deadline has not changed;

insurance premiums calculated on the amount of the payer’s income exceeding RUB 300,000. for the billing period, are now paid by the payer no later than July 1 of the year following the expired billing period. Previously, they had to be paid no later than April 1 of the following year.

The calculation of insurance premiums has not been submitted: new grounds.

Federal Law No. 335-FZ amended paragraph. 2 clause 7 art. 431 of the Tax Code of the Russian Federation, thereby changing the grounds when the calculation of insurance premiums will be recognized as unsubmitted. These innovations come into force on January 1, 2018.

According to the changes made, the calculation of insurance premiums will be considered not submitted if the following indicators for the billing (reporting) period and (or) for each of the last three months of the billing (reporting) period contain errors, as well as if in the calculation submitted by the payer the sums of the same indicators for all individuals do not correspond to the same indicators for the insurance premium payer as a whole:

information for each individual on the amount of payments and other remuneration in favor of individuals - column 210 of the calculation;

the basis for calculating insurance premiums for compulsory health insurance within the established limit value - column 220 of the calculation;

the amount of insurance premiums for health insurance, calculated on the basis of the base for calculating insurance premiums for health insurance, not exceeding the maximum value - column 240 of the calculation;

the basis for calculating insurance premiums for compulsory health insurance at an additional rate is column 280 of the calculation;

the amount of insurance premiums for compulsory health insurance at an additional rate - column 290 of the calculation.

Also, the total indicators in the listed columns for all individuals must correspond to the summary data in subsection. 1.1 and 1.3 sections. 1 calculation.

There remains such a basis as unreliable personal data identifying insured individuals.

The tax authority, as before, will send the payer a corresponding notification that the settlement has not been submitted no later than the day following the day of receipt of the settlement in electronic form (10 days following the day of receipt of the settlement on paper).

A number of changes have been made to Chapter 34 “Insurance Premiums” of the Tax Code of the Russian Federation, which must be taken into account when calculating and paying insurance premiums, as well as submitting calculations for insurance premiums in 2018. Innovations were adopted in order to stimulate investment activity on the territory of the Russian Federation, as well as maintain an economically justified level of fiscal burden for paying insurance premiums, including for individual entrepreneurs.

“On the maximum value of the base for calculating insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity and for compulsory pension insurance from January 1, 2018.”

“On amendments to Article 426 of Part Two of the Tax Code of the Russian Federation.”

“On the Special Economic Zone in the Kaliningrad Region and on amendments to some legislative acts of the Russian Federation.”

Payers of insurance premiums are defined in Art. 419 of the Tax Code of the Russian Federation. Deductions within the framework of various types of compulsory insurance must be made by all employers in relation to the accrued amounts of income of hired personnel, as well as by entrepreneurs who transfer contributions “for themselves”. Based on employee earnings and individual entrepreneurs’ income, tariffs and the algorithm for calculating amounts payable vary significantly. We talked about how insurance premium reporting should be submitted in 2018 in an article on the website earlier, and here we will look at the insurance premium rates in force in 2018.

The legislation establishes obligations to transfer the following insurance premiums:

- to replenish the resources of the pension system;

- for the distribution of funds within the social insurance system (repayment of amounts for sick leave and other benefits);

- on compulsory medical insurance, which gives citizens the right to use a range of free medical services;

- in the Social Insurance Fund - in case of injuries in the workplace and occupational diseases (the only type of contribution that remained under the jurisdiction of the Fund and did not come under the influence of the tax authorities).

| Payer category | Tax base | Bid | Note | |

|---|---|---|---|---|

| An employer (legal entity or individual entrepreneur) making contributions for hired personnel | Pension Fund contributions (2018) | The total value of an individual's taxable income since the beginning of the current year is within 1,021,000 rubles. | 22% | |

| The amount of income exceeding the limit equal to RUB 1,021,000. | 10% | |||

| Social insurance contributions | Taxable income of an individual not exceeding RUB 815,000 from the beginning of the year. | 2,9% | ||

| Income of an individual exceeding the limit of 815,000 rubles. | not taxed | |||

| Income of a foreign citizen or an individual who does not have citizenship temporarily staying in the Russian Federation (within 815,000 rubles) | 1,8% | |||

| Health insurance premiums | Taxable income of employees (without additional upper limit) | 5,1% | ||

| Contributions for “injuries” | Income of individuals subject to insurance premiums | 0,2-8,5% | A total of 32 groups of tariff rates, set depending on the pro-free class | |

| Individual entrepreneur paying contributions “for himself” | Fixed “pension” contributions | The annual income of individual entrepreneurs is within 300 thousand rubles. | RUB 26,545.00 | The rate of contributions to the Pension Fund in 2018 does not depend on the minimum wage and is set at a fixed amount. |

| Individual entrepreneur income exceeding the annual limit of 300 thousand rubles. | 1% | The maximum limit on the total contribution of an individual entrepreneur to pension insurance is 212,360 rubles. (26,545 x 8) | ||

| Fixed premiums for health insurance | Annual income of individual entrepreneurs | RUB 5,840.00 | The tariff does not depend on the minimum wage and is set at a fixed amount |

Preferential rates

Benefits on insurance premiums under the simplified tax system in 2018 are provided to business entities in the form of reduced rates. For some “simplers” there are special tariff values for deductions from the income of hired personnel:

- for “pension” insurance contributions – 20%;

- for contributions to health and social insurance – 0%.

Insurance premiums under the simplified tax system in 2018 can be reduced to preferential rates for legal entities and individual entrepreneurs if their main activity corresponds to the list specified in paragraph 5 of paragraph 1 of Art. 427 Tax Code of the Russian Federation. An additional requirement is that at least 70% of the total income must come from the main type of business activity, and the annual allowable amount of income is limited to an upper limit of 79 million rubles. Similar benefits can be applied by non-profit and charitable structures operating under the simplified tax system with any taxable object.

The same rate of contributions to the Pension Fund in 2018 on preferential terms can be established for business entities operating in the field of pharmacy and using UTII. A similar insurance premium rate is provided for certain types of activities of individual entrepreneurs on a patent (clause 9, clause 1, article 427 of the Tax Code of the Russian Federation). Social and medical insurance contributions and insurance contributions to the Pension Fund in 2018 can also be made on preferential terms by the persons listed in Table 2:

| Payer category | Direction of insurance transfers | Bid, % |

|---|---|---|

|

Pension Fund (percentage of contributions in 2018 by income of employees) | 13 |

| 2,9 | ||

| 1,8 | ||

| Compulsory medical insurance | 5,1 | |

| Legal entities operating in the field of information technology, engaged in the development and adaptation of software products | pension contributions | 8 |

| social insurance | 2 | |

| social insurance of foreign citizens | 1,8 | |

| health insurance | 4 | |

| Participants of the Skolkovo project | Pension Fund | 14 |

| Compulsory medical insurance and social insurance | 0 | |

| Organizations that pay wages to crew members of ships listed in the Russian International Register of Ships | all types of contributions | 0 |

Legal entity and individual entrepreneur with status:

|

Pension Fund | 6 |

| social insurance | 1,5 | |

| Compulsory medical insurance | 0,1 | |

| Russian organizations producing animation products | Pension Fund | 8 |

| social insurance deductions from the earnings of citizens of the Russian Federation | 2 | |

| social insurance contributions from the income of persons with foreign citizenship | 1,8 | |

| compulsory health insurance | 4 |

Additional rates

For pension insurance Art. 428 of the Tax Code of the Russian Federation allocates an additional tariff rate. When calculating these contributions, there is no limitation on the level of taxable income.

For employers who have not conducted a special assessment of working conditions at their workplaces, the rate, depending on the category of personnel and the type of work performed, is equal to:

- 6% - for workers in heavy work (List No. 2 and “small” lists - clauses 2-18, part 1, article 30 of Law No. 400-FZ);

- 9% - for those working in underground conditions, “hot” shops, etc. (List No. 1 - clause 1, part 1, article 30 of the law of December 28, 2013 No. 400-FZ).

If a special assessment has been carried out, the amount of the additional tariff will depend on the assigned hazard class; it can vary in the range from 0% (for the class of optimal and permissible conditions) to 8% (in relation to workplaces with a high level of hazard):

- 8% - 4th level of hazardous working conditions;

- 7% - harmful level, subclass 3.4;

- 6% - harmful level, subclass 3.3;

- 4% - harmful level, subclass 3.2;

- 2% - harmful level, subclass 3.1.;

- 0% - tariff for classes 1 and 2 of the optimal and acceptable level.

Insurance premiums under GPC agreements

If a GPC agreement has been concluded with a person, taxes and contributions for 2018 must be calculated and paid according to the following algorithm:

- Personal income tax is withheld by the tax agent, provided that the performer of the work is an individual (not an individual entrepreneur). In this case, the recipient of the income can, by writing an application to the employer, exercise the right to a professional deduction in the amount of documented expenses associated with the performance of work and services under the GPC agreement (Article 221 of the Tax Code of the Russian Federation).

- Contributions for pension and health insurance are paid if (clause 1 of Article 420 of the Tax Code of the Russian Federation):

- the subject of the contract is the performance of work or provision of services;

- a copyright contract has been concluded;

- under the agreement, the rights to works of literary, musical, artistic direction, or to a scientific work are transferred.

- Social insurance contributions under GPC agreements are not accrued or paid unless this is specifically specified in the agreement.